Trading Crude Oil Under Political Supply Control: How OPEC+, Inventories and Geopolitical Risk Disrupt Normal Price Discovery

The oil market is changing. Unlike the early days of crude oil trading, traditional commodity pricing mechanisms based on the balance between supply and demand are gradually giving way to political, speculative and external factors. OPEC+, global inventory levels and geopolitical risks are creating an environment in which prices do not reflect fundamentals alone, but are shaped by government decisions, investor perception and sudden external shocks.

This article examines how OPEC+ decisions, inventory dynamics and geopolitical tensions translate into oil price movements, and whether fundamentals or market reactions to them play the dominant role in shaping prices today.

The information in this article is provided for educational purposes only and does not constitute financial advice. Consult a financial advisor before making investment decisions.

Is OPEC+ a Group That Controls the Market?

The Organization of the Petroleum Exporting Countries, known as OPEC, was founded in 1960 in Baghdad by five countries: Iran, Iraq, Kuwait, Saudi Arabia and Venezuela, with other members gradually joining later. For decades, the cartel played a central role in shaping supply and influencing oil prices.

But following the sharp price collapse in 2014 caused by the US shale revolution and rapid supply growth from non-OPEC producers, it became clear that the organization alone was no longer able to stabilise the market effectively.

In response, a historic agreement was reached in 2016 with Russia and ten other non-cartel producers, forming the expanded OPEC+ coalition. Today, OPEC+ accounts for roughly 40% of global crude oil production and holds the majority of the world’s proven reserves, making the group one of the most influential actors in the global energy market.

It is also important that many of these countries are relatively flexible producers, meaning they can increase or reduce output fairly quickly thanks to spare production capacity and state control over national oil giants. The most prominent example is Saudi Arabia, often described as a swing producer because it acts as the market’s largest stabiliser.

The group’s price influence mechanism appears simple in theory but is highly complex in practice. When the market faces oversupply and downward price pressure, OPEC+ cuts production quotas, limiting crude availability and supporting prices. Conversely, during periods of shortage and rapid price increases, the group may raise output to ease supply tensions and reduce excessive volatility.

In theory, the mechanism is based on supply management. In practice, market expectations are equally important, as announcements of production cuts or increases often trigger price reactions even before actual volume changes occur. As a result, OPEC+ influence operates not only through physical supply but also through shaping investor sentiment and expectations. Importantly, members are not always aligned, and conflicts sometimes emerge. The most memorable example was the disagreement between Russia and Saudi Arabia over responses to the COVID-19 shock, which led to the price war declared by Saudi Arabia in April 2020 and a subsequent collapse in prices.

Inventories and the Role of China, a New Market Dynamic

The classical rule states that rising oil inventories exert downward pressure on prices, while declining inventories tend to support price increases. In the past, this relationship was relatively transparent, and commercial inventory levels in the United States or OECD countries were one of the main indicators of market equilibrium.

In recent years, however, this relationship has changed significantly. First, the phenomenon of floating storage has grown strongly, meaning crude oil stored on tankers at sea. Such storage usually involves oil originating from sanctioned countries that cannot be sold through official channels. Restrictions on trade with Venezuela, Iran or Russia have resulted in nearly 100 million barrels of sanctioned crude remaining stored on water.

Second, the structure of Chinese demand has changed markedly. One of the most important lessons of recent years is that China has become an even stronger marginal buyer. The country reacts not only to excessively high prices by reducing purchases, but also to low prices by aggressively increasing imports. As a result, alongside Saudi Arabia as a swing producer, China has emerged as a kind of swing demander.

Chinese demand is not a simple function of consumption or refinery margin economics. Domestic refinery decisions are largely subordinated to price control policies, the reduction of fuel subsidy costs and strategic inventory accumulation rather than short-term profitability maximisation.

It is also worth noting that China continues to build strategic stocks. Although Chinese authorities do not formally separate strategic and commercial inventories, and the nature of their refining system blurs the boundary between them, Chinese oil inventories exceeded 1.2 billion barrels in February 2026. In 2025 alone, China imported several hundred thousand barrels per day above refinery requirements. These additional barrels were used to build inventories rather than reflecting a lack of demand. In practice, this creates enormous incremental demand driven not by current consumption but by state-level strategic decisions.

In an article published by the Oxford Institute for Energy Studies titled “Unpacking the ‘Oil Glut’ Narrative: Insights from Stock Dynamics” in September 2025, the authors concluded that the correlation between prompt Brent prices and regional oil inventories has weakened after the COVID period, when the relationship was much stronger. This suggests that inventory levels currently carry less informational value for short-term price movements, especially outside OECD countries.

Geopolitics and the Political Risk Premium

Geopolitical events remain an important driver of short-term oil price volatility, particularly when they threaten the free flow of crude near so-called chokepoints, meaning key logistical bottlenecks. Recent years have brought several such incidents. Houthi attacks on commercial vessels in the Red Sea region, earlier disruptions in major shipping straits, the war in Ukraine and growing tensions in the Persian Gulf have all immediately raised perceived supply risk. Sometimes direct attacks target production facilities rather than transport routes. A notable example occurred in September 2019, when an attack on the Abqaiq and Khurais facilities in Saudi Arabia temporarily removed nearly 6 million barrels per day of production from the market and triggered a sharp price surge.

Although in many cases, the market operates with a so-called political premium, meaning an additional price component reflecting supply concerns that do not always correspond to a lasting physical shortage. If market fundamentals such as high inventory levels or available spare capacity remain comfortable, this premium tends to fade over time. The market prices risk immediately but often discounts it just as quickly when the threat does not materialise into a persistent deficit.

It is also important to note that such shocks often trigger unconventional policy responses. One example was the large-scale release of crude from the US Strategic Petroleum Reserve following the outbreak of the Ukraine war, reaching about 1 million barrels per day for 180 days in an effort to ease price pressure and stabilise the market. Administrative interventions of this type also influence supply balances and market expectations.

In the current environment, geopolitical tensions can be further amplified by financial market mechanics. A developed options market means that rising demand for hedging pushes implied volatility higher, while delta hedging forces option writers to dynamically adjust their futures positions. As a result, price movements can be temporarily magnified by market structure itself, independently of the actual scale of physical disruptions.

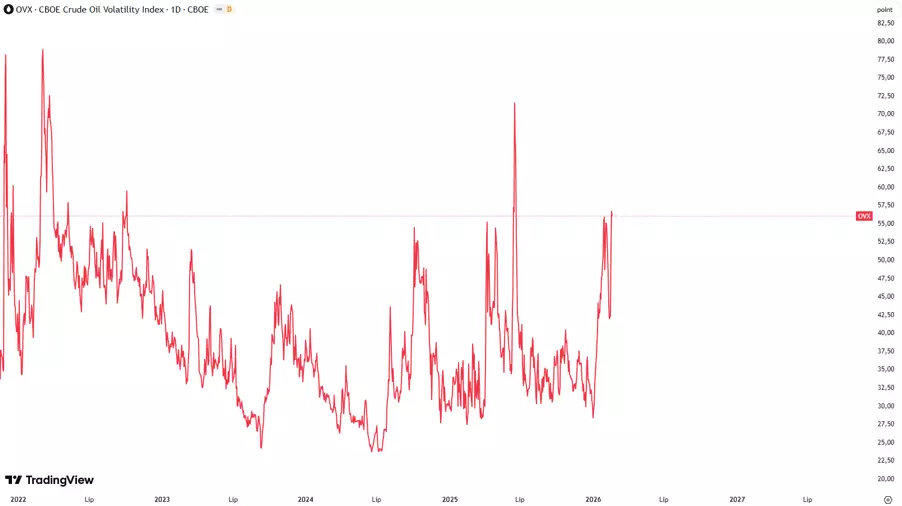

The OVX index serves as a useful indicator for observing this risk premium. OVX is the implied volatility index of oil options and is often referred to as the fear gauge of the oil market. Rising OVX values signal increasing volatility expectations and greater uncertainty among market participants, typically accompanying episodes of geopolitical tension. A sudden jump in OVX while fundamentals remain relatively stable may indicate that fear dominates oil pricing, and under favourable conditions this component tends to gradually dissipate. OVX is usually interpreted relative to its historical average. Values above 40–50 points suggest extreme fear and possible price exhaustion, while levels below 20–25 points indicate market calm. The index is calculated from option prices on the United States Oil Fund (USO), using a 30-day implied volatility model.

Is Market Perception More Important Than the Actual State of Fundamentals?

Finally, it is worth remembering that the fundamental factors discussed above must be interpreted with caution, as the oil market under current conditions does not respond to them in a mechanically linear way. Decisions such as OPEC+ policy shifts, inventory changes, geopolitical tensions or structural supply and demand adjustments influence prices primarily through how they are perceived by market participants.

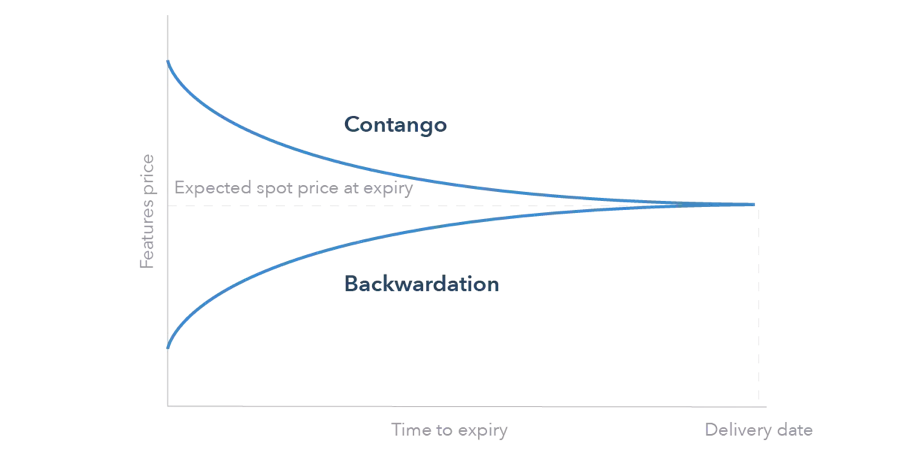

Market reactions may also depend on whether the market is in backwardation or contango. In backwardation, when spot prices are higher than forward prices, storage incentives are limited and supply pressure tends to translate more quickly into price movements. In contrast, in contango, when forward prices exceed spot prices, the market encourages inventory accumulation, which can dampen short-term price impulses and slow the reaction to individual fundamental signals.

This means that what matters is not only the occurrence of a fundamental event itself, but also how it influences investor expectations, positioning and the market reaction function. Consequently, the scale and durability of price responses depend more on perception and market structure than on the fundamental shock alone.

The given data provides additional information regarding all analysis, estimates, prognosis, forecasts, market reviews, weekly outlooks or other similar assessments or information (hereinafter “Analysis”) published on the websites of Admirals investment firms operating under the Admirals trademark (hereinafter “Admirals”) Before making any investment decisions please pay close attention to the following: