DAX30 CFD price action should stay calm as long as the trade war does

Source: Economic Events Calendar November 11 – 15, 2019 - Admiral Markets' Forex Calendar

DAX30 CFD

Already into the start of last week, the German DAX30 CFD made it back above 13,000 points, falling short to re-test the May/June highs 2018 in the region around 13,200/230 points, broke above and that said stabilised above 13,000 points over the last week.

While we still don't see a deep correction, we are still becoming a little careful in regards to significant further gains on the upside, too.

Since the economic calendar is quite thin in the days to come, we have the feeling that tensions between the US and China in regards to their current Phase-1 trade-deal negotiations could start to re-gain momentum any time soon.

On Thursday, the Chinese Commerce Ministry said that China and the US have agreed to cancel existing tariffs in different phases and if China and the US reach a Phase 1 Trade Deal, both sides must cancel existing tariffs at the same time with the same proportion based on the agreement.

Still, we have the feeling that especially the rising pressure on US president Trump in regards to the current impeachment developments, could result in the Chinese using these developments as a tool to build further pressure on the US and Trump, telling them to give up on all already imposed tariffs, else they won't negotiate further on the Phase-1-deal or anything which will follow.

We remember that after Trump attacked the Chinese despite contrary arrangements with Xi Jinping in Osaka at the G20 summit by imposing new tariffs at the 01st of August, we could imagine the Chinese using the impeachment developments and the current political headwinds Trump faces in the US as a tool to build pressure on Trump, telling him to reduce/giving up on the already imposed tariffs, else they won't negotiate further on the Phase-1-deal or anything which will follow.

Such developments could trigger a correction in the DAX30 CFD, but given the recent and very dovish stances from the ECB and Fed, it seems difficult to see a sustainable break back below 13,000 points.

Nevertheless, if such a drop occurs, a push down to 12,470/500 stays an option.

Still, as long as the German index trades above its SMA(200), the mode stays clearly bullish and a Santa-Clause rally with a DAX30 CFD closing 2019 above 13,000 points stays on the table:

Source: Admiral Markets MT5 with MT5-SE Add-on DAX30 CFD Daily chart (between August 2, 2018, to November 8, 2019). Accessed: November 8, 2019, at 10:00pm GMT - Please note: Past performance is not a reliable indicator of future results, or future performance.

In 2014, the value of the DAX30 CFD increased by 2.65%, in 2015, it increased by 9.56%, in 2016, it increased by 6.87%, in 2017, it increased by 12.51%, in 2018, it fell by 18.26%, meaning that after five years, it was up by 10.5%.

Check out Admiral Markets' most competitive conditions on the DAX30 CFD and Dow Jones CFDs and start trading on the DAX30 CFD with a low 0.8 point spread offering during the main Xetra trading hours!

US Dollar

After the Fed cut, as expected, rates by 25 basis points on October 30, but didn't deliver any significant further impulses or signs in regards to future monetary policy steps, the "data dependent" part in the Fed statement.

Here, the Fed removed the sentence "Will Act As Appropriate" and replaced it with a more data-dependent one "Will Monitor Implications of Incoming Information for the economic outlook as it assesses the appropriate path of the target range for the fed funds rate".

As a result market participants were obviously left speculating that the Fed won't deliver any dovish hints or a looser monetary policy in the next months.

"Obviously", because in the first days of November 10-year US-Treasury yields took on bullish momentum, gained over 20 basis points while nearly another Fed rate cut was nearly completely priced-out for the rate decision in December.

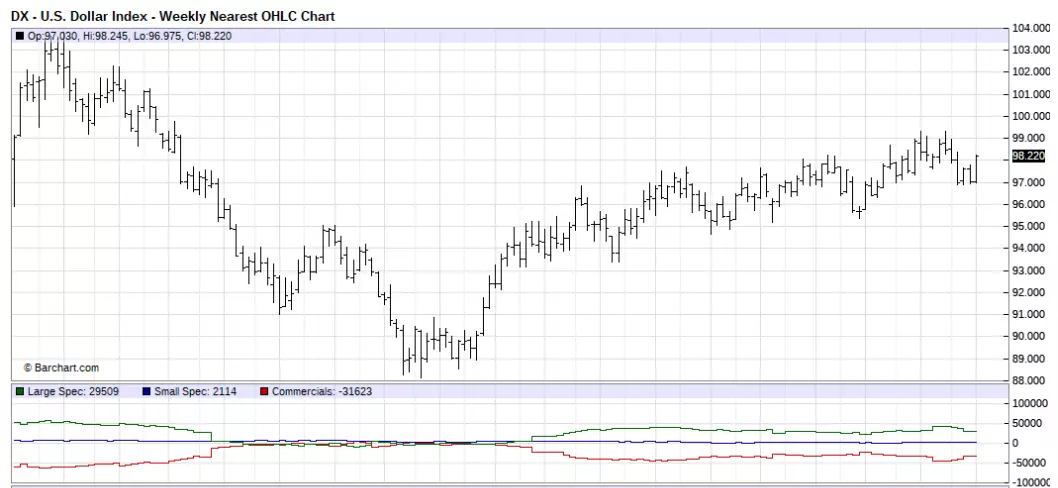

As a result, the USD Index Future regained all losses which occurred after the Fed's rate decision, but still we remain sceptical for the US dollar into at least the end of the year 2019.

This is now mainly due to the fact that there is still also the option on the table that we get to see an extension of the recent announced "Non-QE"-QE program, where the current plan is to buy US Treasuries for the next 8.5 months at a pace of 60 billion USD per month and if there are any hints of rising tensions in the money respectively repo market again, the Fed could consider an extension of her "Non-QE"-QE program.

With that in mind, the US dollar stays a potential short candidate, even though from a technical perspective the sequence of higher highs and lows stays intact as long as the USD Index Future stays above 95.00 points on a weekly time frame:

Source: Barchart - U.S Dollar Index - Weekly Nearest OHLC Chart (between May 2016 to October 2019). Accessed: 08 November 2019 at 10:00 PM GMT

Don't forget to register for the weekly "Trading Spotlight" webinar with presenters including Jens Klatt, every Monday, Wednesday and Friday at 2pm London time! It's your opportunity to follow Jens and others as they explore the weekly market outlook in detail, so don't miss out!

Euro

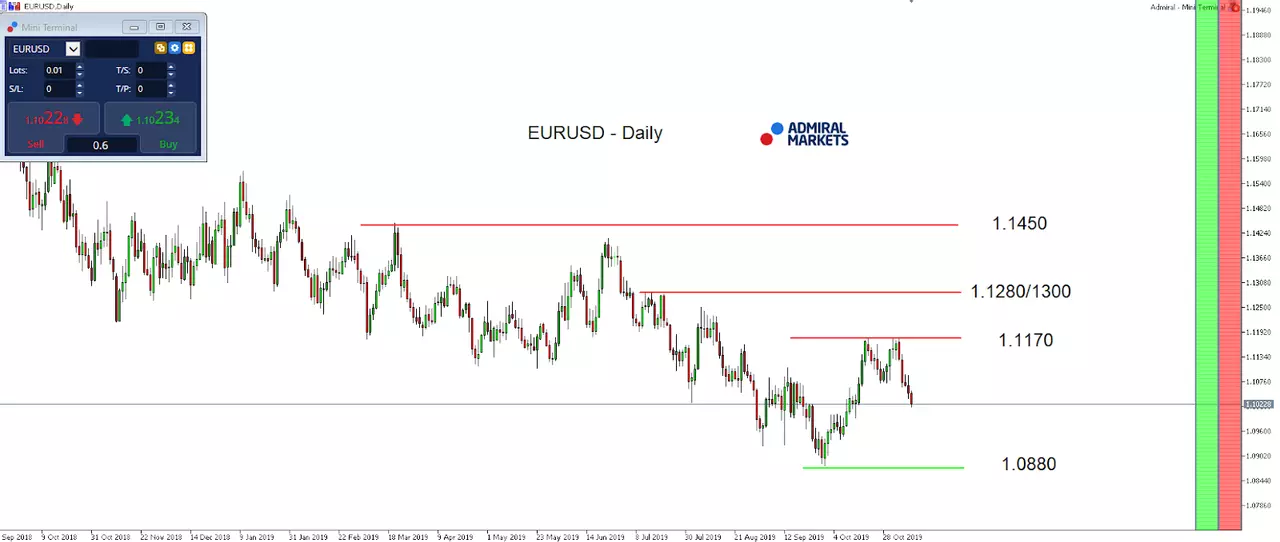

As we expected in our last weekly market outlook, the overall picture in the Euro hasn't significantly changed over the last few days, but remains dependent on the developments in the US dollar and here especially in US yields.

Still and even if Draghi successor Christine Lagarde is only ECB president for a few days, signs intensify that tensions are building between the ECB and especially Germany.

Lagarde told a German newspaper that "Germany is just one of 19 countries in the euro zone and the European Central Bank needs all of them to be "on board" with its policy decisions", which seems unlikely given the recent QE-ternity announcement in September and Germany (beside France, Netherlands, Austria and Estonia) not being d'accord with this decision.

While we still don't see any Euro-volatility driving announcement being made in the upcoming days, we still favour further gains in the Euro with a first target around 1.1280/1300, while a breakthrough levels the path up to 1.1400 in the weeks to come, not only due to US dollar weakness, but probably also due to rising speculation of Germany sooner, rather than later, deviate from its current path and favour fiscal stimulus, too.

This outlook would only be negated with EUR/USD dropping sustainably back below 1.1000:

Source: Admiral Markets MT5 with MT5-SE Add-on EUR/USD Daily chart (between September 17, 2018, to November 8, 2019). Accessed: November 8, 2019, at 10:00pm GMT - Please note: Past performance is not a reliable indicator of future results, or future performance.

In 2014, the value of the EURUSD fell by 11.9%, in 2015, it fell by 10.2%, in 2016, it fell by 3.2%, in 2017, it increased by 13.92%, 2018, it fell by 4.4%, meaning that after five years, it was down by 16.5%.

JPY

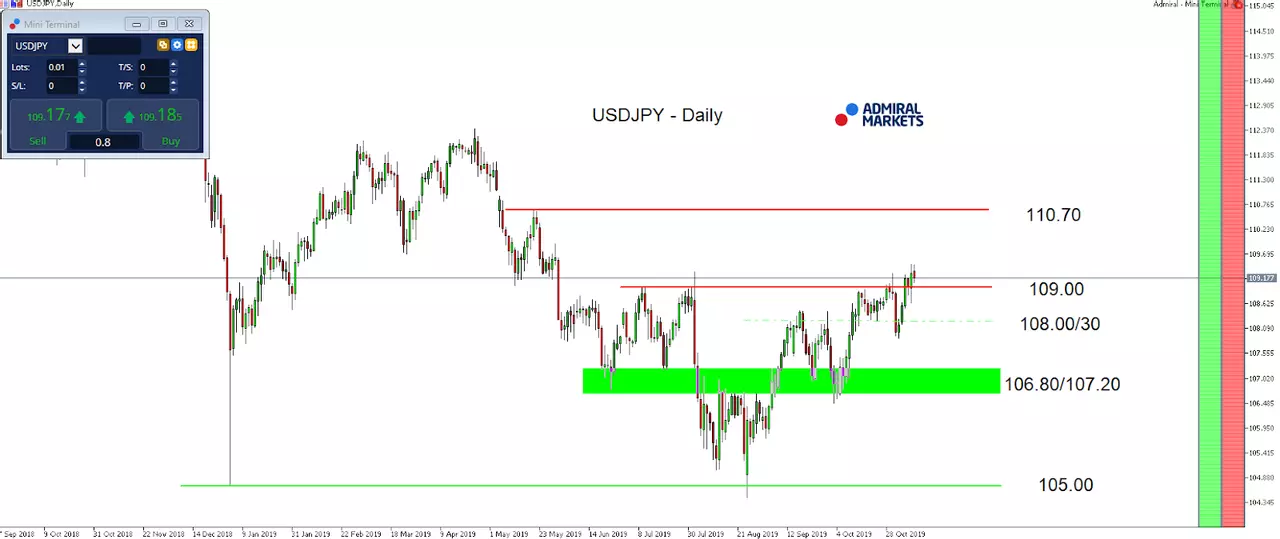

In our last weekly market outlook we stated, that […]as a result (note: not only in regards to the Fed and mixed US economic data, but especially in regards to the BoJ rate decision and only slight change in her forward guidance), we see the advantage in USD/JPY in the days to come on the short-side with our make-or-break-level around 108.00/30.[…]

When looking at the USD/JPY daily chart, we can clearly see that this call was wrong.

Instead, the USD/JPY held above 107.80/108.00 and pushed back towards 109.30, mainly driven by 10-year US-Treasury yields which took on bullish momentum, gained over 20 basis points and drove the positive correlated USD/JPY higher, too.

Interesting enough, we made also such a bullish scenario a topic, but only in a side noted which ended the following way: […]chances of a sustainable break higher remain low in our opinion.[…]

And this outlook has in fact not changed. The reason for that can be found in the already nearly completely priced-in outcome of the Fed rate decision in December that no further rate cut will be announced.

This could change if the next economic projection from the US come in worse than expected, but also if tensions between the US and China start to re-gain momentum in regards to their current Phase-1 trade-deal negotiations.

On Thursday, the Chinese Commerce Ministry said that China and the US have agreed to cancel existing tariffs in different phases and if China and the US reach a Phase 1 Trade Deal, both sides must cancel existing tariffs at the same time with the same proportion based on the agreement.

Still, we have the feeling that especially the rising pressure on US president Trump in regards to the current impeachment developments, could result in the Chinese using these developments as a tool to build further pressure on the US and Trump, telling them to give up on all already imposed tariffs, else they won't negotiate further on the Phase-1-deal or anything which will follow.

That said, rising rate-cut-speculation and/or risk-off-fears could result in any spikes above 109.00/30 in USDJPY to be not sustainable, but instead being a fake out, resulting in the USD/JPY going for another stint to the region around 108.00:

Source: Admiral Markets MT5 with MT5-SE Add-on USDJPY Daily chart (between 17 September 2018 to 07 November 2019). Accessed: 07 November 2019 at 10:00 PM GMT - Please note: Past performance is not a reliable indicator of future results, or future performance.

In 2014, the value of the USD/JPY increased by 13.7%, in 2015, it increased by 0.5%, in 2016, it fell by 2.8%, in 2017, it fell by 3.6%, in 2018, it fell by 2.7%, meaning that after five years, it was up by 4.1%.

Gold

After the Fed cut, as expected, rates by 25 basis points on October 30, but didn't deliver any significant further impulses or signs in regards to future monetary policy steps, the "data dependent" part in the Fed statement left market participants obviously speculating that the Fed won't deliver any dovish hints or a looser monetary policy in the next months.

"Obviously", because in the first days of November 10-year US-Treasury yields took ion bullish momentum, gained over 20 basis points.

While Gold could initially stabilise above 1,500 USD (in our opinion a potential sign of inherent strength), the ISM Non-Manufacturing data set last Tuesday, pointing to a rise of 54.7 in October from a near 3-year low of 52.6 in September, beating market expectations of 53.5, the yellow metal dropped sharply back below 1,500 USD with a slight delay.

With expectations among market participants of another Fed rate cut by 25 basis points in December dropping to around 5%, making such a step very unlikely, the bullish outlook for Gold darkened a little.

Only if Gold bulls succeed in breaking above 1,520 USD, another test of the current yearly highs around 1,557 USD would be possible, the mode currently seems short-term bearish.

Nevertheless, the overall technical picture on a daily time-frame didn't significantly darken, but instead brings now a potential mid-term long trigger around 1,440/450 USD into play:

Source: Admiral Markets MT5 with MT5-SE Add-on Gold Daily chart (between August 10, 2018, to November 8, 2019). Accessed: November 8, 2019, at 10:00pm GMT - Please note: Past performance is not a reliable indicator of future results, or future performance.

In 2014, the value of Gold fell by 1.7%, in 2015, it fell by 10.4%, in 2016 it increased by 8.1%, in 2017 it increased by 13.1%, in 2018, it fell by 1.6%, meaning that after five years, it was up by 6.4%.

Discover the world's #1 multi-asset platform

Admiral Markets offers professional traders the ability to trade with a custom, upgraded version of MetaTrader 5, allowing you to experience trading at a significantly higher, more rewarding level. Experience benefits such as the addition of the Market Heat Map, so you can compare various currency pairs to see which ones might be lucrative investments, access real-time trading data, and so much more. Click the banner below to start your FREE download of MT5 Supreme Edition!

Disclaimer: The given data provides additional information regarding all analysis, estimates, prognosis, forecasts or other similar assessments or information (hereinafter "Analysis") published on the website of Admiral Markets. Before making any investment decisions please pay close attention to the following:

- This is a marketing communication. The analysis is published for informative purposes only and are in no way to be construed as investment advice or recommendation. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and that it is not subject to any prohibition on dealing ahead of the dissemination of investment research.

- Any investment decision is made by each client alone whereas Admiral Markets shall not be responsible for any loss or damage arising from any such decision, whether or not based on the Analysis.

- Each of the Analysis is prepared by an independent analyst (Jens Klatt, Professional Trader and Analyst, hereinafter "Author") based on the Author's personal estimations.

- To ensure that the interests of the clients would be protected and objectivity of the Analysis would not be damaged Admiral Markets has established relevant internal procedures for prevention and management of conflicts of interest.

- Whilst every reasonable effort is taken to ensure that all sources of the Analysis are reliable and that all information is presented, as much as possible, in an understandable, timely, precise and complete manner, Admiral Markets does not guarantee the accuracy or completeness of any information contained within the Analysis. The presented figures refer that refer to any past performance is not a reliable indicator of future results.

- The contents of the Analysis should not be construed as an express or implied promise, guarantee or implication by Admiral Markets that the client shall profit from the strategies therein or that losses in connection therewith may or shall be limited.

- Any kind of previous or modeled performance of financial instruments indicated within the Publication should not be construed as an express or implied promise, guarantee or implication by Admiral Markets for any future performance. The value of the financial instrument may both increase and decrease and the preservation of the asset value is not guaranteed.

- The projections included in the Analysis may be subject to additional fees, taxes or other charges, depending on the subject of the Publication. The price list applicable to the services provided by Admiral Markets is publicly available from the website of Admiral Markets.

- Leveraged products (including contracts for difference) are speculative in nature and may result in losses or profit. Before you start trading, you should make sure that you understand all the risks.