FED delivers as expected: Santa Claus rally in the making?

This week's weekly market outlook will provide insights for DAX30 CFD, the US Dollar, the Euro, the Japanese Yen and Gold, following last week's FED release and in the lead up to this years Santa Claus rally.

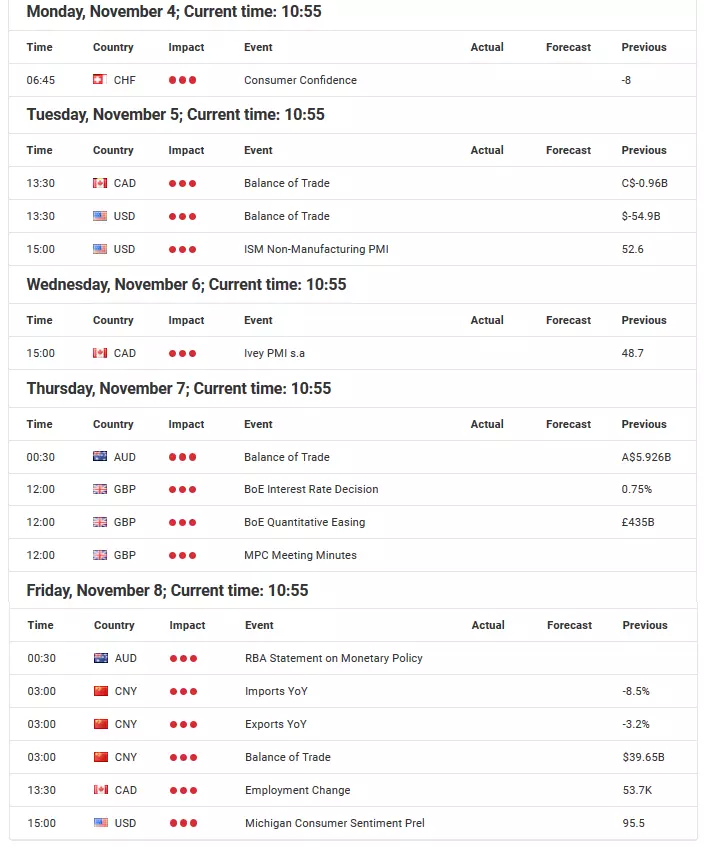

Source: Economic Events Calendar 04 November – 08 November 2019 - Admiral Markets' Forex Calendar

DAX30 CFD

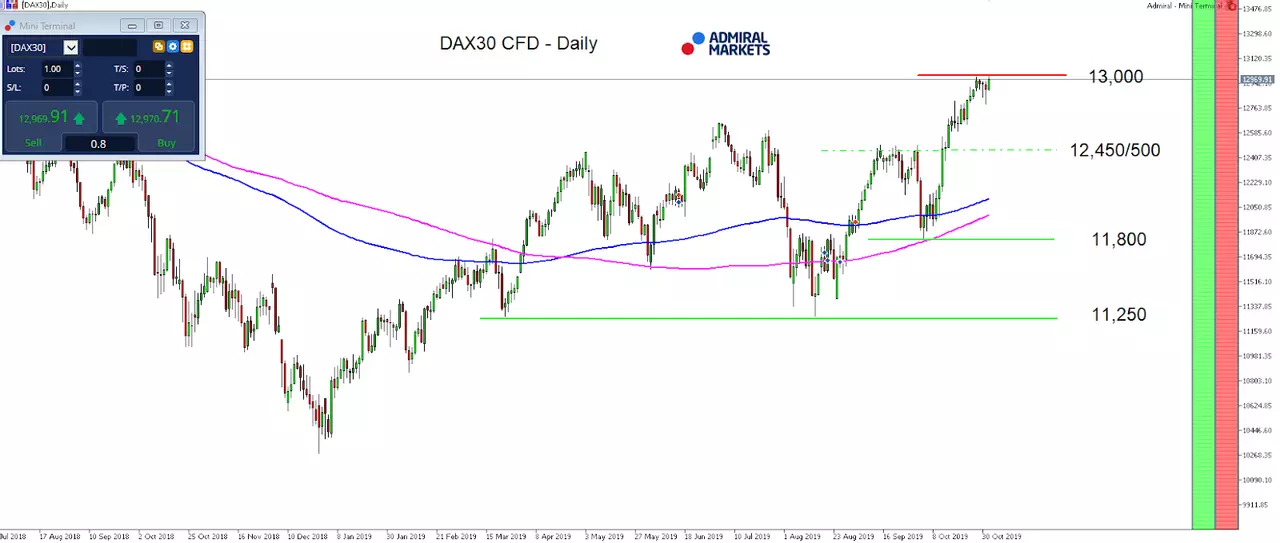

As we covered in our last weekly market outlook for the DAX30 CFD: another stint up to 12,900 points, but significant and further gains back above 13,000 points don't seem very likely.

And indeed, the bulls failed short to at least take a slight glance above 13,000 points, but only traded as high as 12,992 points.

Given the fact that the FED delivered, as expected, a rate cut of 25 basis points and kept the door open for further monetary stimulus (not only in regards to another 0.25% rate cut at the December meeting, but also in delivering further liquidity to the repo market in her "Non-QE" QE program), our take for the upcoming days is similar to last week.

While we are still being careful about expecting significant further gains in the German index and a push above 13,000 points, we don't see a deep correction either.

A retracement down to 12,470/500 stays an option, but as long as the German index trades above its SMA(200), the mode stays bullish.

The reason for our scepticism in regards to increasing volatility is that it's difficult to see equities come under serious pressure in the near-term due to the massive liquidity being delivered by the US central bank.

That said, intraday short-engagement should be conservatively traded while the region around 12,450/500 could be of interest for long engagement aiming on trading a Santa Claus rally:

Source: Admiral Markets MT5 with MT5SE Add-on DAX30 CFD Daily chart (between 26 July 2018 to 01 November 2019). Accessed: 01 November 2019 at 10:00 PM GMT

Please note: Past performance is not a reliable indicator of future results, or future performance.

In 2014, the value of the DAX30 CFD increased by 2.65%, in 2015, it increased by 9.56%, in 2016 it increased by 6.87%, in 2017 it increased by 12.51%, in 2018 it fell by 18.26%, meaning that after five years, it was up by 10.5%.

Check out Admiral Markets' most competitive conditions on the DAX30 CFD and Dow Jones CFDs and start trading on the DAX30 CFD with a low 0.8 point spread offering during the main Xetra trading hours!

US dollar

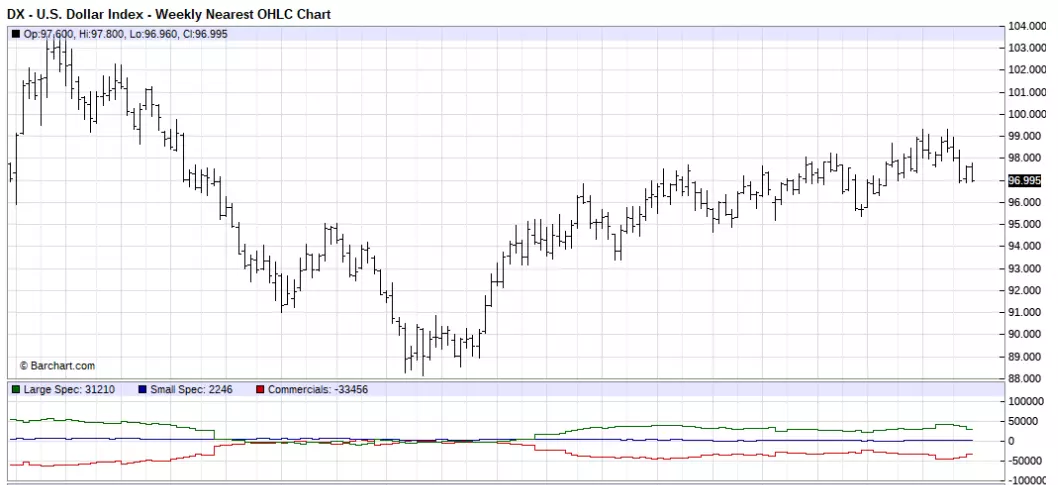

After the FED cut, as expected, rates by 25 basis points last Wednesday, but didn't deliver any significant further impulses or signs in regards to future monetary policy steps (which resulted in a stabilisation of expectations around another 0.25% cut in December among market participants initially at around 20%), the ISM Manufacturing PMI printed at 48.3 points for October, rising slightly from a decade-low of 47.8 points, but still missing market expectations of 48.9 points, keeping near-term recession fears in the US elevated.

Since the FED removed in her statement the sentence "Will Act As Appropriate" and replaced it with a more data-dependent one "Will Monitor Implications of Incoming Information for the economic outlook as it assesses the appropriate path of the target range for the fed funds rate", our outlook for the US dollar stays sceptical.

This is not only because of another rate cut in December due to mixed to bad US economic data. In addition, there is the option of an extension to the recently announced "Non-QE" QE program.

The current plan is to buy US Treasuries for the next 8.5 months at a pace of 60 billion USD per month and if there are any hints of rising tensions in the money respectively repo market again with the FED considering an extension of her "Non-QE" QE program, the US-Dollar stays a potential short candidate.

This seems especially true since the FED Watch Tool currently points to only a 10% chance of another 25 basis points rate cut at the December meeting, having some potential to rise in the days to come. This could be driven by the ISM Non-Manufacturing data release on Tuesday, which is continuing to show further signs of weakness. In September, for example, the data set slumped to 52.6, coming in well below market expectations of 55.0 points, showing the lowest reading since August 2016, with firms mostly concerned about tariffs, labour resources and the direction of the economy.

Still, from a technical perspective the sequence of higher highs and lows stays intact as long as the USD Index Future stays above 95.00 points on a weekly time frame.

Source: Barchart - U.S Dollar Index - Weekly Nearest OHLC Chart (between May 2016 to October 2019). Accessed: 01 November 2019 at 10:00 PM GMT

Don't forget to register for the weekly "Trading Spotlight" webinar with presenters including Jens Klatt, every Monday, Wednesday and Friday at 2pm London time. It's your opportunity to follow Jens and others as they explore the weekly market outlook in detail, so don't miss out!

Euro

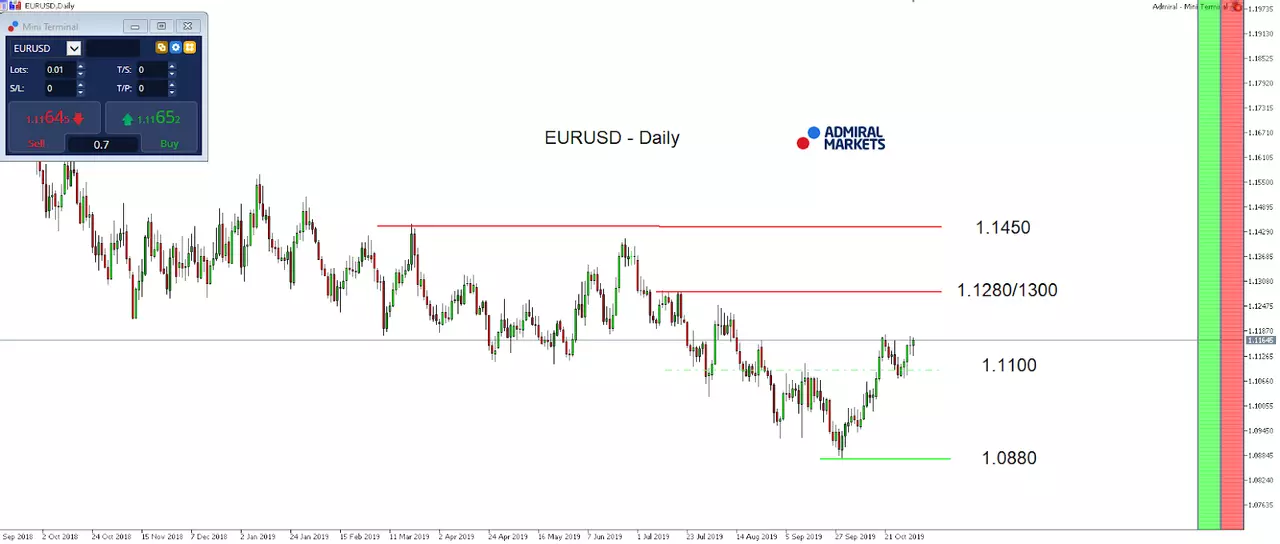

Compared to last week, our take for the Euro hasn't changed.

Last Monday, Christine Lagarde took over the position as ECB president from Mario Draghi, and we do not expect any significant monetary announcements, similar to the light monetary policy decision on October 24.

The main drivers in the EURUSD currency pair will be in our opinion the Brexit farce (which is likely to lose some/most of its influence after the next UK election on December 12) and especially the developments around the US dollar and US yields after the latest FED rate decision.

So, given our scepticism around the US dollar and the obvious sustainable break back and consolidation above 1.1100 in EURUSD, we favour further gains in the Euro with a first target around 1.1280/1300, while a breakthrough levels the path up to 1.1400 in the weeks to come.

Source: Admiral Markets MT5 with MT5SE Add-on EURUSD Daily chart (between 03 September 2018 to 01 November 2019). Accessed: 01 November 2019 at 10:00 PM GMT

Please note: Past performance is not a reliable indicator of future results, or future performance.

In 2014, the value of the EURUSD fell by 11.9%, in 2015, it fell by 10.2%, in 2016 it fell by 3.2%, in 2017 it increased by 13.92%, 2018 it fell by 4.4%, meaning that after five years, it was down by 16.5%.

JPY

The highly anticipated FED and BoJ rate decision didn't trigger significant volatility, but USDJPY nevertheless stays, in our opinion, a very attractive currency pair for traders on the short side.

After the FED cut, as expected, rates by 25 basis points last Wednesday, but didn't deliver any significant further impulses or signs in regards to future monetary policy steps (which resulted in a stabilisation of expectations around another 0.25% cut in December among market participants initially at around 20%), the ISM Manufacturing PMI printed at 48.3 points for October, rising slightly from a decade-low of 47.8 points, but still missing market expectations of 48.9 points, keeping near-term recession fears in the US elevated.

The BoJ on the other hand didn't deliver anything new (or especially 'dovish' after the latest dovish stances from the FED and ECB) after reviewing their previous monetary policy meetings, but remained, after the latest signs of a (partial) trade deal between the US and China, in a 'wait-and-see' mode.

While the Japanese Central Bank tweaked her forward guidance (and to some extent delivered at least something dovish to not disappoint the expectations of market participants), it also communicated that it felt that the Japanese economy was strong enough without the need for direct additional easing.

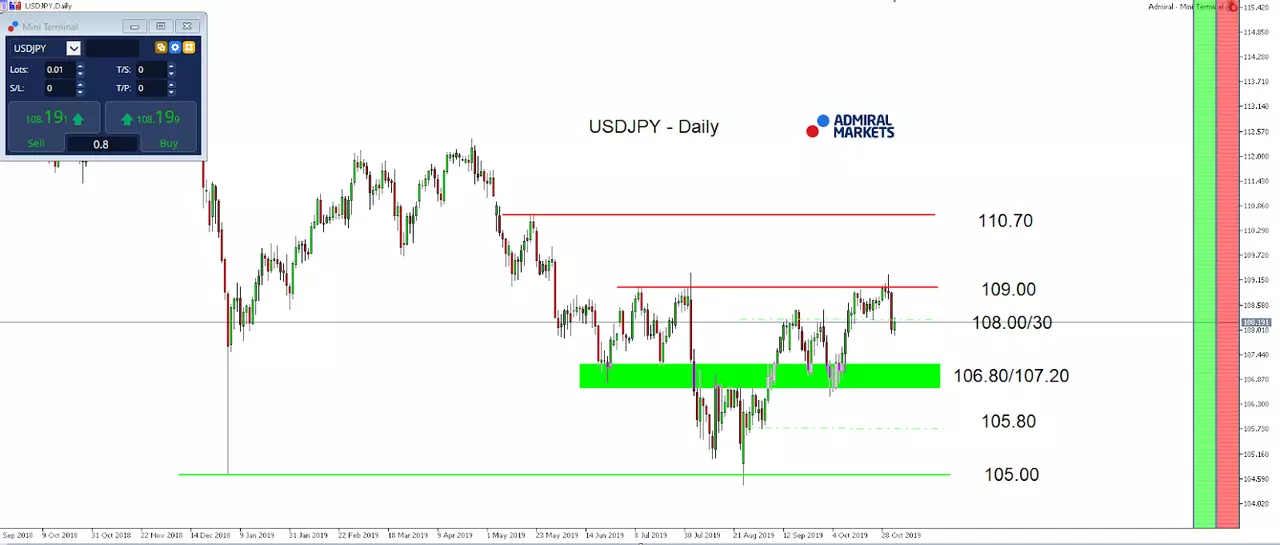

As a result, we see the advantage in USDJPY in the days to come on the short-side with our make-or-break-level around 108.00/30. A break below activates 106.80/107.00 as a next target.

On the other hand: if the US dollar sees some stabilisation while an increasing risk-on among market participants and resulting JPY selling enters the market, we could see another attack of the region around 109.00, even though chances of a sustainable break higher remain low in our opinion.

Source: Admiral Markets MT5 with MT5SE Add-on USDJPY Daily chart (between 14 September 2018 to 01 November 2019). Accessed: 01 November 2019 at 10:00 PM GMT

Please note: Past performance is not a reliable indicator of future results, or future performance.

In 2014, the value of USDJPY increased by 13.7%, in 2015, it increased by 0.5%, in 2016 it fell by 2.8%, in 2017 it fell by 3.6%, in 2018 it fell by 2.7%, meaning that after five years, it was up by 4.1%.

Gold

After the FED cut, as expected, rates by 25 basis points last Wednesday, but didn't deliver any significant further impulses or signs in regards to future monetary policy steps (which resulted in a stabilisation of expectations around another 0.25% cut in December among market participants initially at around 20%), the ISM Manufacturing PMI printed at 48.3 points for October, rising slightly from a decade-low of 47.8 points, but still missing market expectations of 48.9 points, keeping near-term recession fears in the US elevated.

As a result, Gold pushed back and closed above 1,500 USD last week. Given the recent fundamental developments and especially the outlook for the expected monetary policy path of the FED (meaning that the FED will act more data-dependent in regards to her future rate cut policy), our stance remains bullish for the yellow metal.

This is especially true, if the ISM Non-Manufacturing data set on Tuesday continues to show signs of weakness.

If Gold bulls succeed in breaking above 1,520 USD, another test of the current yearly highs around 1,557 USD seems only a question of time.

On the other hand a short-term drop below the October lows around 1,460 USD wouldn't darken the picture, but instead bring a potential mid-term long trigger around 1,440/450 USD into play.

Source: Admiral Markets MT5 with MT5SE Add-on Gold Daily chart (between 27 July 2018 to 01 November 2019). Accessed: 01 November 2019 at 10:00 PM GMT

Please note: Past performance is not a reliable indicator of future results, or future performance.

In 2014, the value of Gold fell by 1.7%, in 2015, it fell by 10.4%, in 2016 it increased by 8.1%, in 2017 it increased by 13.1%, in 2018, it fell by 1.6%, meaning that after five years, it was up by 6.4%.

Disclaimer: The given data provides additional information regarding all analysis, estimates, prognosis, forecasts or other similar assessments or information (hereinafter "Analysis") published on the website of Admiral Markets. Before making any investment decisions please pay close attention to the following:

- This is a marketing communication. The analysis is published for informative purposes only and are in no way to be construed as investment advice or recommendation. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and that it is not subject to any prohibition on dealing ahead of the dissemination of investment research.

- Any investment decision is made by each client alone whereas Admiral Markets shall not be responsible for any loss or damage arising from any such decision, whether or not based on the Analysis.

- Each of the Analysis is prepared by an independent analyst (Jens Klatt, Professional Trader and Analyst, hereinafter "Author") based on the Author's personal estimations.

- To ensure that the interests of the clients would be protected and objectivity of the Analysis would not be damaged Admiral Markets has established relevant internal procedures for prevention and management of conflicts of interest.

- Whilst every reasonable effort is taken to ensure that all sources of the Analysis are reliable and that all information is presented, as much as possible, in an understandable, timely, precise and complete manner, Admiral Markets does not guarantee the accuracy or completeness of any information contained within the Analysis. The presented figures refer that refer to any past performance is not a reliable indicator of future results.

- The contents of the Analysis should not be construed as an express or implied promise, guarantee or implication by Admiral Markets that the client shall profit from the strategies therein or that losses in connection therewith may or shall be limited.

- Any kind of previous or modeled performance of financial instruments indicated within the Publication should not be construed as an express or implied promise, guarantee or implication by Admiral Markets for any future performance. The value of the financial instrument may both increase and decrease and the preservation of the asset value is not guaranteed.

- The projections included in the Analysis may be subject to additional fees, taxes or other charges, depending on the subject of the Publication. The price list applicable to the services provided by Admiral Markets is publicly available from the website of Admiral Markets.

- Leveraged products (including contracts for difference) are speculative in nature and may result in losses or profit. Before you start trading, you should make sure that you understand all the risks.