Will the FED shoot the DAX30 CFD back above 13,000 points?

This week's weekly market outlook will provide insights for DAX30 CFD, the US Dollar, the Euro, the Japanese Yen and Gold, ahead of this week's FED and Non-Farm Payrolls releases, as well as announcements about new quantitative easing programs in the US and Europe.

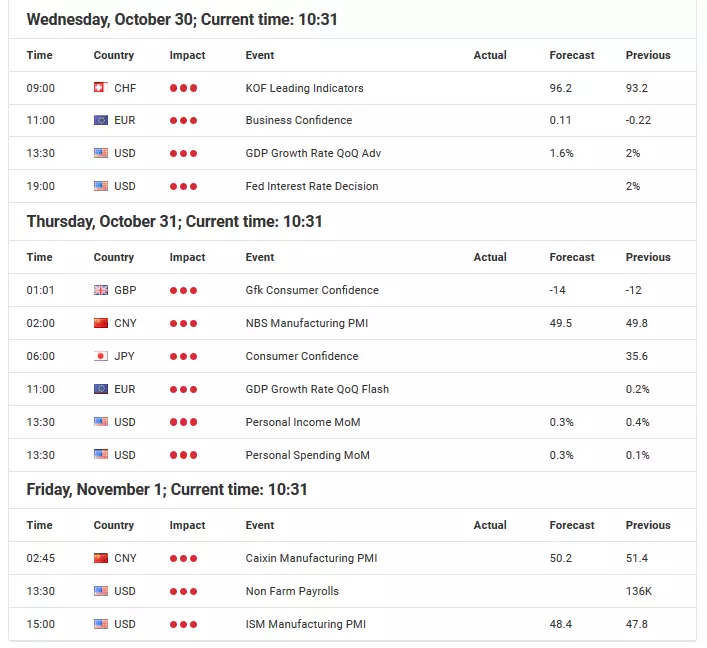

Source: Economic Events Calendar 28 October – 01 November 2019 - Admiral Markets' Forex Calendar

DAX30 CFD

After the DAX30 CFD marked new yearly highs last week but failed to gain further bullish momentum, it is important to be careful about expecting significant further gains in the German index.

While the days before the FED rate decision are statistically known to be bullish for the DAX30 CFD, given the recent developments around the Brexit deal, the light monetary adjustments of the ECB last Thursday and the current US-Chinese trade deal truce, significant and further gains back above 13,000 points don't seem very likely in our opinion.

Since most of the positive effects are already priced in, a retracement down to 12,470/500 is a serious option.

Here we see a potential long trigger against which another stint up to 12,900 points is possible, at least as long as the German index trades above its SMA(200), currently trading around 11,900 points.

On the other hand: given the latest news around the massive liquidity injections from the FED, conducting for example nearly 65 billion USD in overnight repurchase agreements and another 35 billion USD in repo operation last Tuesday alone, it's difficult to see Equities come under serious pressure in the near-term, especially with the FED rate decision taking place on Wednesday.

So, our take is: we'd only take conservative long engagements, since we are not very comfortable given the nearly completely priced in optimism around the US-Chinese trade and Brexit deal, while the political uncertainty around the Trump impeachment remains, but see Equities solidly supported thanks to the stabilising central banks around the globe:

Source: Admiral Markets MT5 with MT5SE Add-on DAX30 CFD Daily chart (between 19 July 2018 to 25 October 2019). Accessed: 25 October 2019 at 10:00 PM GMT

Please note: Past performance is not a reliable indicator of future results, or future performance.

In 2014, the value of the DAX30 CFD increased by 2.65%, in 2015, it increased by 9.56%, in 2016 it increased by 6.87%, in 2017 it increased by 12.51%, in 2018 it fell by 18.26%, meaning that after five years, it was up by 10.5%.

Check out Admiral Markets' most competitive conditions on the DAX30 CFD and start trading on the DAX30 CFD with a low 0.8 point spread offering during the main Xetra trading hours!

US Dollar

The upcoming days in the US dollar will be mainly driven by the FED rate decision on Wednesday and the Non-Farm Payrolls release, especially the ISM Manufacturing data release, on Friday.

While a rate cut of 25 basis points is nearly completely priced in (currently the FED Watch Tool shows a likelihood of over 90%), what's certainly of higher interest is the rhetoric in regards to the rate decision in December and the announced "Non-QE"-QE program.

Here, the current plan is to buy US Treasuries for the next 8.5 months at a pace of 60 billion USD per month and any hints at Wednesday's meeting that the FED could consider extending that program if no improvement in regards to the liquidity issue in the repo market is seen, the US Dollar could see a next wave of heavier selling.

This seems especially true since the FED Watch Tool points to only a 30% chance of another 25 basis points rate cut at the December meeting.

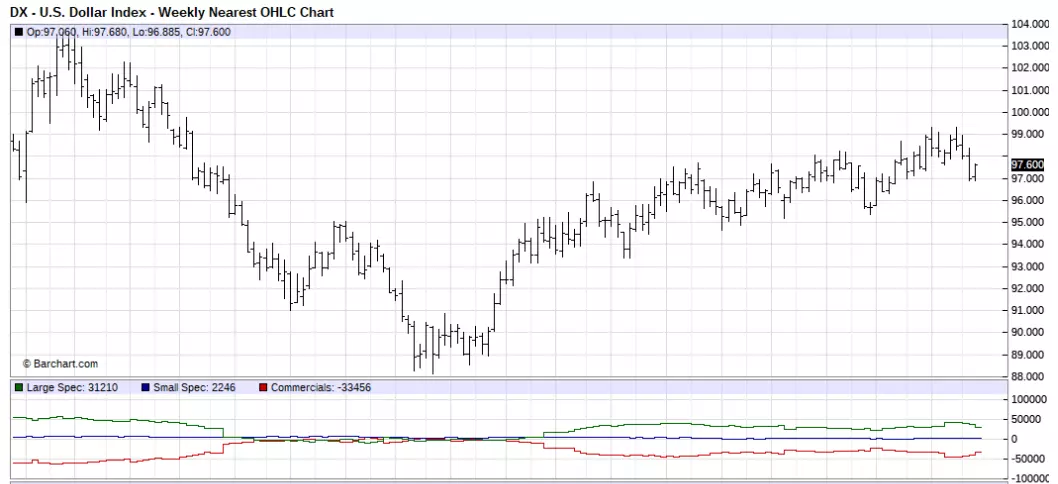

If in addition to such a dovish rhetoric, the US economic releases, especially the ISM Manufacturing on Friday, continue to trend lower (for September the ISM Manufacturing dropped to 47.8, the steepest contraction in the manufacturing sector since June 2009). Consequently, the technically crucial support region around 95.00 points could come under pressure in the USD Index Future.

Source: Barchart - U.S Dollar Index - Weekly Nearest OHLC Chart (between May 2016 to October 2019). Accessed: 25 October 2019 at 10:00 PM GMT

Don't forget to register for the weekly "Trading Spotlight" webinar with presenters including Jens Klatt, every Monday, Wednesday and Friday at 2pm London time! It's your opportunity to follow Jens and others as they explore the weekly market outlook in detail, so don't miss out!

Euro

Last week's focus was certainly on the last press conference under the moderation of Mario Draghi, who left as the president of the Governing Council after it became clear that the QE decision in September was opposed by at least seven top ECB officials.

All in all, the meeting last Thursday was light on monetary adjustments after the ECB announced the re-start of the QE program at a pace of €20bn per month on September 12, saying that the program would run for as long as necessary.

Since journalists haven't significantly pressure Draghi on details on the building tensions after the latest QE decision, volatility in the European currency will most likely be driven in the upcoming weeks (until the first press conference under the moderation of Christine Lagarde) by the developments in the US dollar and Brexit.

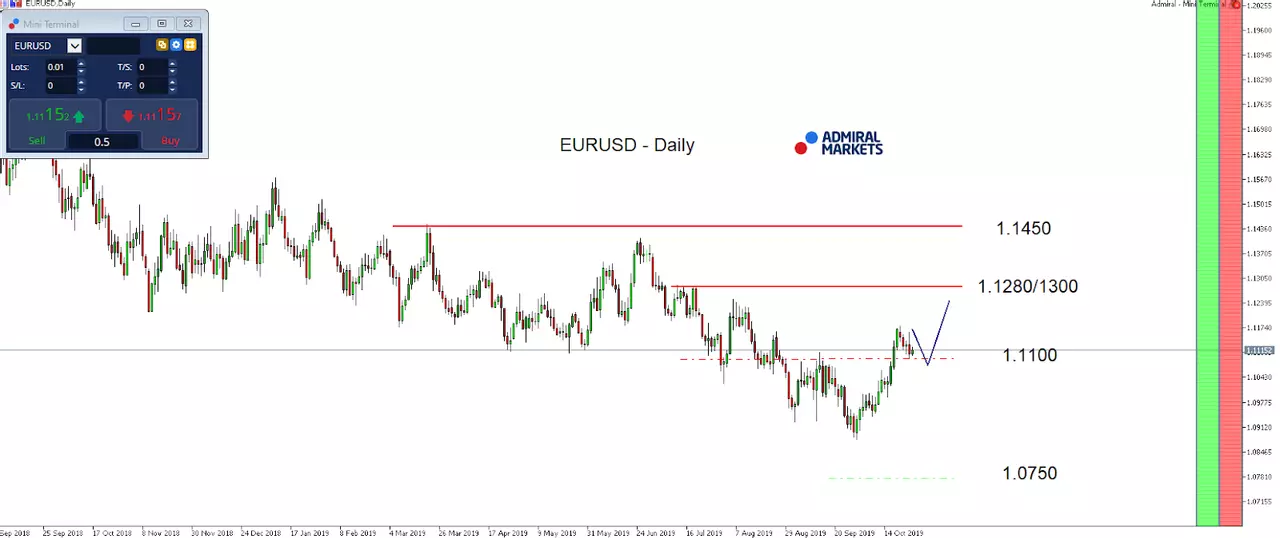

Especially given our bearish USD outlook in the paragraph above and the sustainable break back above 1.1100 in EURUSD, we favour further gains in the Euro with a first target around 1.1280/1300, while a breakthrough levels the path up to 1.1400.

Source: Admiral Markets MT5 with MT5SE Add-on EURUSD Daily chart (between 03 September 2018 to 25 October 2019). Accessed: 25 October 2019 at 10:00 PM GMT

Please note: Past performance is not a reliable indicator of future results, or future performance.

In 2014, the value of the EURUSD fell by 11.9%, in 2015, it fell by 10.2%, in 2016 it fell by 3.2%, in 2017 it increased by 13.92%, 2018 it fell by 4.4%, meaning that after five years, it was down by 16.5%.

JPY

The upcoming days in USDJPY will be mainly driven by the FED rate decision on Wednesday and the BoJ rate decision on Thursday.

While a FED rate cut of 25 basis points is nearly completely priced in, what's certainly of higher interest is the rhetoric in regards to the rate decision in December and the announced "Non-QE"-QE program.

Here, the current plan is to buy US Treasuries for the next 8.5 months at a pace of 60 billion USD per month. Any hints at Wednesday's meeting that the FED could consider extending that program could result in a wave of heavier selling in the US dollar, resulting out of another push lower in 10-year US yields, going for another test of the region around the all time lows at 1.36%.

If in addition to such a dovish FED rhetoric, it will be interesting to see what the BoJ delivers, especially after the recent turbulences in Japanese bond markets where 10-year JGB yields spiked on October 2 after a poorly received auction. This is a likely sign that traders are finally paying heed to Kuroda's recent comments warning against excessive falls in super-long yields, and leaving us with expectations that the BoJ is to deliver a more dovish stance than currently expected.

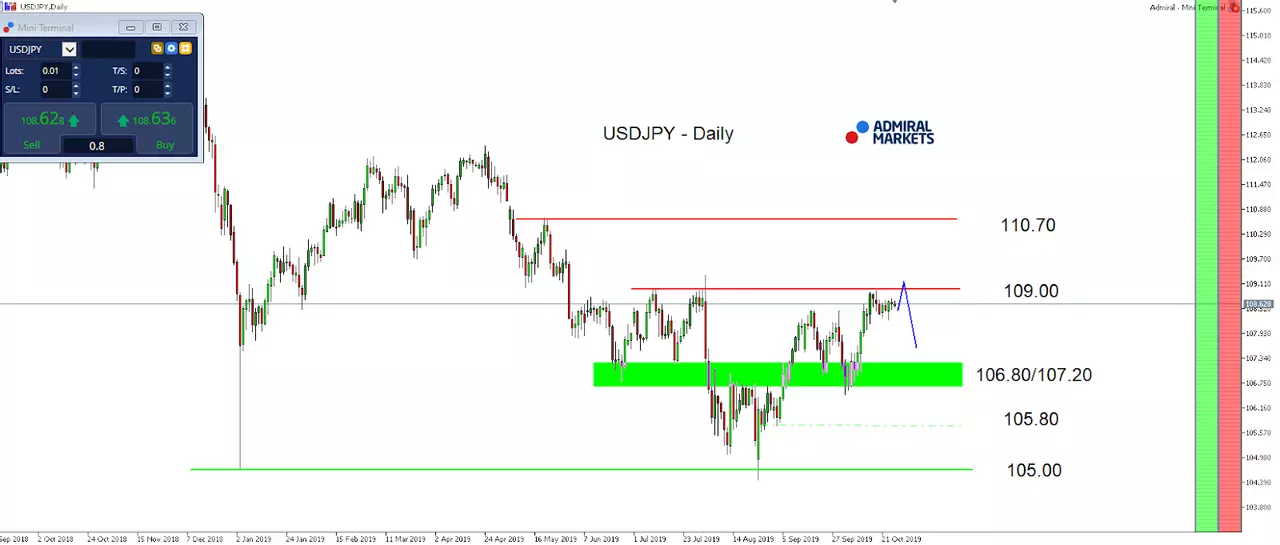

If the latter expectation around the BoJ is not fulfilled while the FED delivers dovish rhetoric, and if US economic releases continue to disappoint, a sustainable break above 109.00 seems unlikely.

Instead another attempt to break back below 106.80/107.00 remains a serious possibility, even though USDJPY is technically neutral on a daily time-frame between 106.80/107.00 and 108.50/109.00.

Source: Admiral Markets MT5 with MT5SE Add-on USDJPY Daily chart (between 10 September 2018 to 25 October 2019). Accessed: 25 October 2019 at 10:00 PM GMT

Please note: Past performance is not a reliable indicator of future results, or future performance.

In 2014, the value of USDJPY increased by 13.7%, in 2015, it increased by 0.5%, in 2016 it fell by 2.8%, in 2017 it fell by 3.6%, in 2018 it fell by 2.7%, meaning that after five years, it was up by 4.1%.

Gold

The overall picture in Gold hasn't significantly changed over the last week of trading, but we are in good spirits that this will change over the coming days.

The upcoming days will be mainly driven by the FED rate decision on Wednesday and the Non-Farm Payrolls release, probably especially the ISM Manufacturing data release, on Friday.

While a rate cut of 25 basis points is nearly completely priced in, what's certainly of higher interest is the rhetoric in regards to the rate decision in December and the announced "Non-QE"-QE program.

Here, the current plan is to buy US Treasuries for the next 8.5 months at a pace of 60 billion USD per month and any hints at Wednesday's meeting that the FED could consider extending that program if no improvement in regards to the liquidity issue in the repo market is seen, Gold could take on bullish momentum again and recapture 1,500 USD with US yields expected to push lower again.

If in addition to such a dovish rhetoric the US economic releases, especially the ISM Manufacturing release on Friday, continue to trend lower and result in rising recession fears (for September the ISM Manufacturing dropped to 47.8, the steepest contraction in the manufacturing sector since June 2009). This means the yellow metal has a solid chance of making an attack at the region around 1,520 USD.

In general and from a technical perspective, the advantage in Gold stays on the Long side above 1,380 USD and our mid-term target around 1,650/700 USD is still active.

And again: even a stint below the current October lows around 1,460 USD wouldn't darken the picture, but instead bring a potential mid-term long trigger around 1,440/450 USD into play:

Source: Admiral Markets MT5 with MT5SE Add-on Gold Daily chart (between 27 July 2018 to 25 October 2019). Accessed: 25 October 2019 at 10:00 PM GMT

Please note: Past performance is not a reliable indicator of future results, or future performance.

In 2014, the value of Gold fell by 1.7%, in 2015, it fell by 10.4%, in 2016 it increased by 8.1%, in 2017 it increased by 13.1%, in 2018, it fell by 1.6%, meaning that after five years, it was up by 6.4%.

Disclaimer: The given data provides additional information regarding all analysis, estimates, prognosis, forecasts or other similar assessments or information (hereinafter "Analysis") published on the website of Admiral Markets. Before making any investment decisions please pay close attention to the following:

- This is a marketing communication. The analysis is published for informative purposes only and are in no way to be construed as investment advice or recommendation. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and that it is not subject to any prohibition on dealing ahead of the dissemination of investment research.

- Any investment decision is made by each client alone whereas Admiral Markets shall not be responsible for any loss or damage arising from any such decision, whether or not based on the Analysis.

- Each of the Analysis is prepared by an independent analyst (Jens Klatt, Professional Trader and Analyst, hereinafter "Author") based on the Author's personal estimations.

- To ensure that the interests of the clients would be protected and objectivity of the Analysis would not be damaged Admiral Markets has established relevant internal procedures for prevention and management of conflicts of interest.

- Whilst every reasonable effort is taken to ensure that all sources of the Analysis are reliable and that all information is presented, as much as possible, in an understandable, timely, precise and complete manner, Admiral Markets does not guarantee the accuracy or completeness of any information contained within the Analysis. The presented figures refer that refer to any past performance is not a reliable indicator of future results.

- The contents of the Analysis should not be construed as an express or implied promise, guarantee or implication by Admiral Markets that the client shall profit from the strategies therein or that losses in connection therewith may or shall be limited.

- Any kind of previous or modeled performance of financial instruments indicated within the Publication should not be construed as an express or implied promise, guarantee or implication by Admiral Markets for any future performance. The value of the financial instrument may both increase and decrease and the preservation of the asset value is not guaranteed.

- The projections included in the Analysis may be subject to additional fees, taxes or other charges, depending on the subject of the Publication. The price list applicable to the services provided by Admiral Markets is publicly available from the website of Admiral Markets.

- Leveraged products (including contracts for difference) are speculative in nature and may result in losses or profit. Before you start trading, you should make sure that you understand all the risks.