Thanksgiving should weigh heavily on volatility, still, bulls should be careful

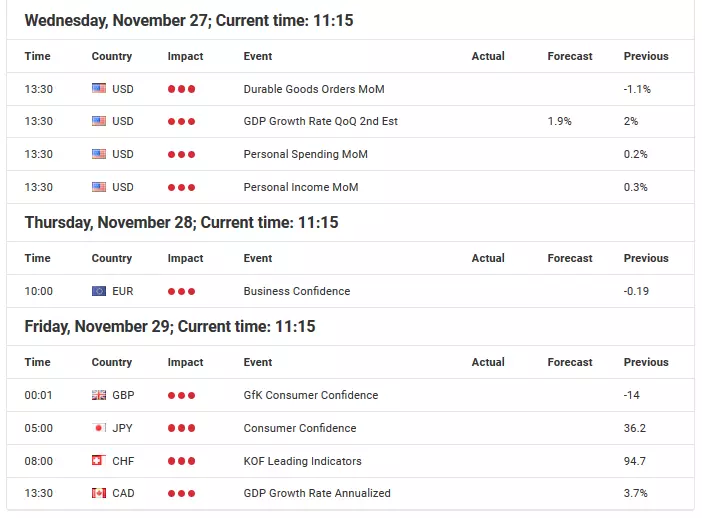

Source: Economic Events Calendar November 25 – 29, 2019 - Admiral Markets' Forex Calendar

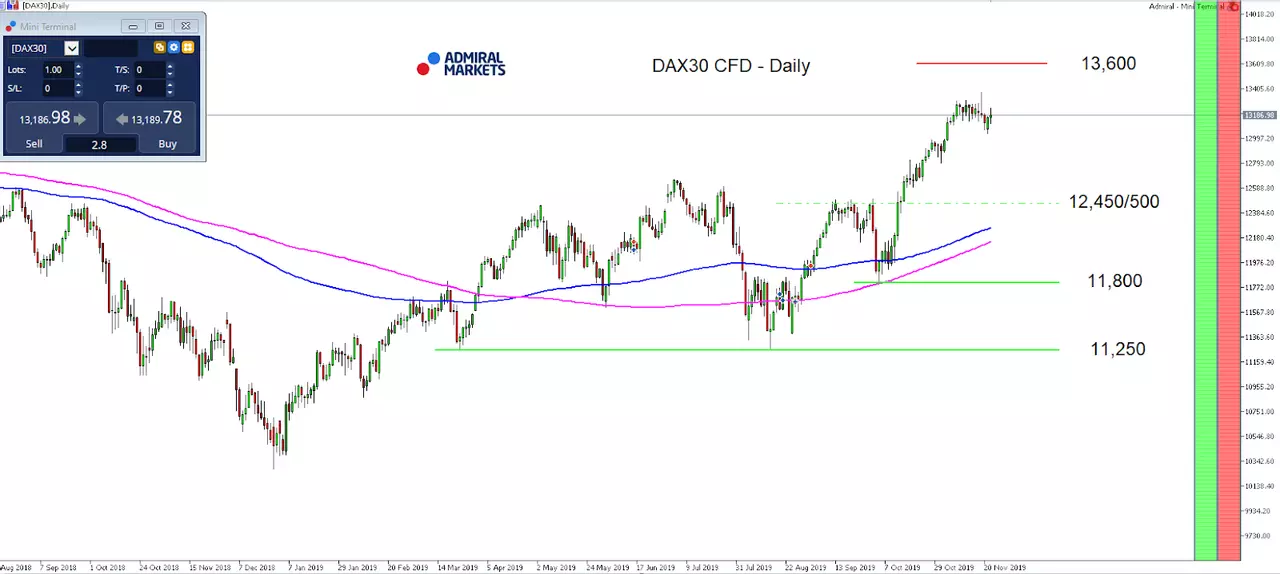

DAX30 CFD

The price action in the DAX30 CFD has been quite interesting over the last week of trading: initially, the German index started volatile into the last week with rising tensions in the trade dispute between the US and China making a test of the region around 13,000 likely.

Here, rumours made rounds that the mood in Beijing about a trade deal is rather pessimistic with the Chinese being more and more troubled after signs intensified that no tariff rollback seems to be on the table (which especially China thought both economies had agreed in principle on) and the strategy now switching to "talk only" and wait due to the recent impeachment developments and uncertainty around the upcoming US election.

Interesting enough, the drop lower was delayed, instead bulls bundled their power on Tuesday, pushing the DAX30 CFD to new yearly highs and above 13,300 points, only to show weakness later that day with bears pushing the index lower and bring the psychological relevant region around 13,000 points into the focus of market participants in the second half of the week.

What our lines outline is, that the mode in DAX30 CFD seems to stay choppy, probably with a slight advantage to be found on the Short-side.

Still, we remain sceptical and do not expect a deeper corrective move, not only because of the thin economic calendar in the days to come, but also Thanksgiving and Black Friday in the days ahead.

The resulting lower than usual volatility and shortened trading hours in US equities reduce chances of sharper moves, especially on the downside.

Nevertheless, bulls shouldn't be too over-confident, too: rising pressure on Trump in the current impeachment hearings and his known erratic behaviour leave chances of comments in regards to the trade dispute between the US and China, but also Europe on the table and can be expected anytime.

Still, given the recent and very dovish stances from the ECB and Fed, it seems difficult to see a sustainable break back below 13,000 points. Even if such a drop occurs, the DAX30 CFD should be solidly supported around 12,470/500 from where a Santa Claus rally with a DAX30 CFD closing 2019 above 13,000 points stays on the table:

Source: Admiral Markets MT5 with MT5-SE Add-on DAX30 CFD Daily chart (between August 16, 2018, to November 22, 2019). Accessed: November 22, 2019, at 10:00pm GMT - Please note: Past performance is not a reliable indicator of future results, or future performance.

In 2014, the value of the DAX30 CFD increased by 2.65%, in 2015, it increased by 9.56%, in 2016, it increased by 6.87%, in 2017, it increased by 12.51%, in 2018, it fell by 18.26%, meaning that after five years, it was up by 10.5%.

Check out Admiral Markets' most competitive conditions on the DAX30 CFD and Dow Jones CFDs and start trading on the DAX30 CFD with a low 0.8 point spread offering during the main Xetra trading hours!

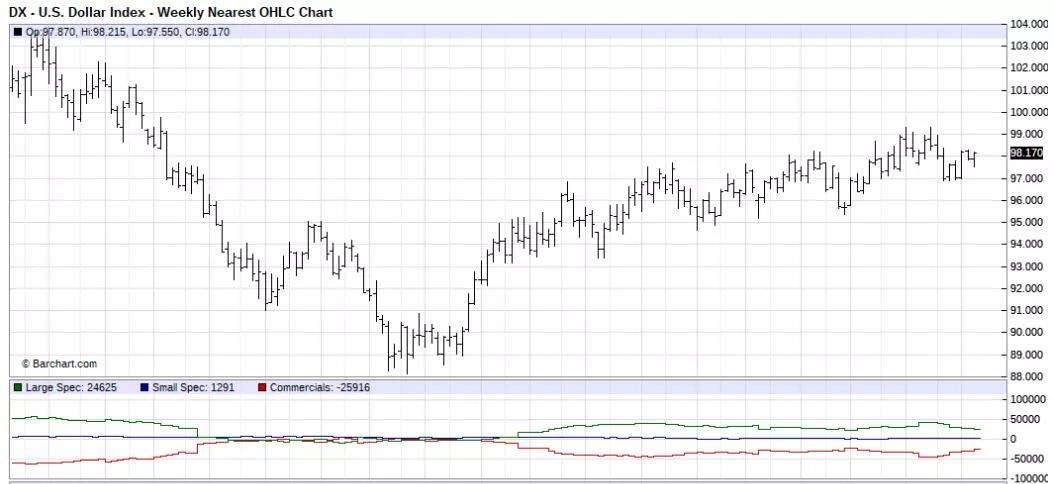

US Dollar

The last week of trading hasn't delivered any new hints in regards to the US dollar and our outlook hasn't changed.

After 10-year US-Treasury yields took on bullish momentum in the first half of November, gaining over 20 basis points and driving the US dollar Index Future higher, over the last days most of these gains were given back.

With the economic calendar being thin in the days to come and Thanksgiving and Black Friday ahead, volatility should stay low, especially in the US dollar which is currently clearly driven by US yields.

Still, we remain sceptical for the US dollar, especially now, where it becomes obvious that the Fed's balance sheet is expanding at a faster rate than during QE1, QE2 or QE3, an overall bearish environment for the Greenback. This is especially true, also short-term, if any signs arise which would increase expectations among market participants of another Fed rate cut by 25 basis points in December which is currently nearly completely priced out according to the Fed Watch Tool.

With that in mind, the US dollar stays a potential short candidate, even though from a technical perspective the sequence of higher highs and lows stays intact as long as the USD Index Future stays above 95.00 points on a weekly time frame:

Source: Barchart - U.S Dollar Index - Weekly Nearest OHLC Chart (between May 2016 to November 2019). Accessed: November 22, 2019, at 10:00pm GMT

Don't forget to register for the weekly "Trading Spotlight" webinar with presenters including Jens Klatt, every Monday, Wednesday and Friday at 2pm London time! It's your opportunity to follow Jens and others as they explore the weekly market outlook in detail, so don't miss out!

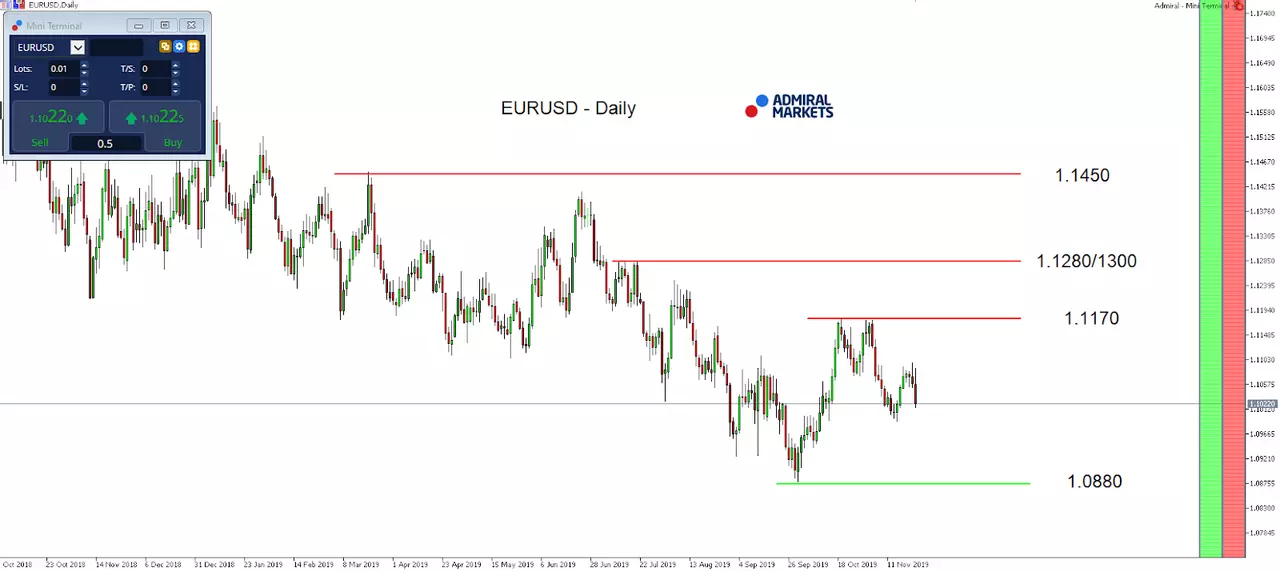

Euro

The picture in the Euro hasn't changed over the course of the last week of trading. While the Euro could stabilise above 1.1000 against the US dollar, it became quite clear that the current main driver can be found in US yields.

With US yields giving back most of their gains of the first two weeks in November, the US dollar lost most of its bullish momentum, too, and thus "helping" the Euro.

While we expect subdued volatility in yields in the days to come, especially with Thanksgiving and Black Friday ahead, and thus don't see big moves in the EUR/USD, we still want to reinforce our careful Euro outlook after the latest comments from US president Trump at his speech at the Economic Club in New York on November 12.

While we still consider the speech to be kind of a pre-election party, significant steps like auto-tariffs for Europe are a serious threat and any such announcement could dynamically drive the Euro significantly lower and sustainably below 1.1000.

Nevertheless, with the Fed's balance sheet currently expanding at a faster rate than during QE1, QE2 or QE3, we still favour the Long-side in the Euro with a first target around 1.1280/1300, while a breakthrough levels the path up to 1.1400 in the weeks to come:

Source: Admiral Markets MT5 with MT5-SE Add-on EUR/USD Daily chart (between October 1, 2018, to November 22, 2019). Accessed: November 22, 2019, at 10:00pm GMT - Please note: Past performance is not a reliable indicator of future results, or future performance.

In 2014, the value of the EUR/USD fell by 11.9%, in 2015, it fell by 10.2%, in 2016, it fell by 3.2%, in 2017, it increased by 13.92%, 2018, it fell by 4.4%, meaning that after five years, it was down by 16.5%.

JPY

While the outlook for the Japanese Yen and particularly the USD/JPY hasn't in fact changed over the last few days (and will likely not change over the next days with Thanksgiving and Black Friday ahead, reducing chances of risk on/off driven moves in yield and currencies, especially in JPY), recent fundamental developments leave us with excitement in regards to the weeks and months ahead.

With the Fed's balance sheet expanding at a faster rate than during QE1, QE2 or QE3, 10-year US-Treasury yields losing their bullish momentum of the first two weeks of November and rumours making rounds that the mood in Beijing about a trade deal is rather pessimistic (=tensions between the US and China rising again), the USD/JPY bears are probably smelling a kind of an advantage in the near-term.

It is said that China is more and more troubled after signs intensified that no tariff rollback seems to be on the table (which especially China thought both economies had agreed in principle on), with the strategy now switching to "talk only" and wait due to the recent impeachment developments around Trump.

In fact, this development is not a big surprise to us (as pointed out in our last weekly market outlook for example), but reinforces our sceptical view on the USD/JPY.

That said, we still consider the Short-side in the USD/JPY to be more attractive from a risk-reward-perspective and don't see the recent spikes above 109.00/30 in USDJPY as sustainable, but instead to be potential fake-outs, resulting in the USD/JPY going for another stint to the region around 107.80/108.00.

Still, given our expectation around a subdued volatility outlook, we don't expect an aggressive attack at the region around 106.80/107.00, at least not for now respectively into the yearly close which would definitely increase chances of a sharper drop from a technical perspective as low as 105.00 and probably even lower:

Source: Admiral Markets MT5 with MT5-SE Add-on USD/JPY Daily chart (between September 14, 2018, to November 22, 2019). Accessed: November 22, 2019, at 10:00pm GMT - Please note: Past performance is not a reliable indicator of future results, or future performance.

In 2014, the value of USD/JPY increased by 13.7%, in 2015, it increased by 0.5%, in 2016, it fell by 2.8%, in 2017, it fell by 3.6%, in 2018, it fell by 2.7%, meaning that after five years, it was up by 4.1%.

Gold

Over the last days, the picture in Gold hasn't significantly changed: after the push below 1,500 USD, mainly driven by the sharp rise in 10-year US-Treasury yields into the start of the month of November, the upcoming days and also the next week with Thanksgiving and Black Friday should present themselves with overall low volatility.

Still, from a fundamental perspective, the outlook for the yellow metal remains positive in our opinion.

With the Fed's balance sheet expanding at a faster rate than during QE1, QE2 or QE3, 10-year US-Treasury yields losing their bullish momentum of the first two weeks of November and rumours making rounds that the mood in Beijing about a trade deal is rather pessimistic (=tensions between the US and China rising again), while into the yearly close a known bullish seasonal window opens, Gold bulls are most likely already champing at the bit, at least behind closed doors.

While technically, our picture switches to Long again with Gold breaking back above 1,520 USD which would level the path up to the current yearly highs around 1,557 USD, a first bullish sign in the lower time-frames (H1) is already sent with Gold recapturing 1,490/495 USD:

Source: Admiral Markets MT5 with MT5-SE Add-on Gold Daily chart (between August 24, 2018, to November 22, 2019). Accessed: November 22, 2019, at 10:00pm GMT - Please note: Past performance is not a reliable indicator of future results, or future performance.

In 2014, the value of Gold fell by 1.7%, in 2015, it fell by 10.4%, in 2016, it increased by 8.1%, in 2017, it increased by 13.1%, in 2018, it fell by 1.6%, meaning that after five years, it was up by 6.4%.

Discover the world's #1 multi-asset platform

Admiral Markets offers professional traders the ability to trade with a custom, upgraded version of MetaTrader 5, allowing you to experience trading at a significantly higher, more rewarding level. Experience benefits such as the addition of the Market Heat Map, so you can compare various currency pairs to see which ones might be lucrative investments, access real-time trading data, and so much more. Click the banner below to start your FREE download of MT5 Supreme Edition!

Disclaimer: The given data provides additional information regarding all analysis, estimates, prognosis, forecasts or other similar assessments or information (hereinafter "Analysis") published on the website of Admiral Markets. Before making any investment decisions please pay close attention to the following:

- This is a marketing communication. The analysis is published for informative purposes only and are in no way to be construed as investment advice or recommendation. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and that it is not subject to any prohibition on dealing ahead of the dissemination of investment research.

- Any investment decision is made by each client alone whereas Admiral Markets shall not be responsible for any loss or damage arising from any such decision, whether or not based on the Analysis.

- Each of the Analysis is prepared by an independent analyst (Jens Klatt, Professional Trader and Analyst, hereinafter "Author") based on the Author's personal estimations.

- To ensure that the interests of the clients would be protected and objectivity of the Analysis would not be damaged Admiral Markets has established relevant internal procedures for prevention and management of conflicts of interest.

- Whilst every reasonable effort is taken to ensure that all sources of the Analysis are reliable and that all information is presented, as much as possible, in an understandable, timely, precise and complete manner, Admiral Markets does not guarantee the accuracy or completeness of any information contained within the Analysis. The presented figures refer that refer to any past performance is not a reliable indicator of future results.

- The contents of the Analysis should not be construed as an express or implied promise, guarantee or implication by Admiral Markets that the client shall profit from the strategies therein or that losses in connection therewith may or shall be limited.

- Any kind of previous or modeled performance of financial instruments indicated within the Publication should not be construed as an express or implied promise, guarantee or implication by Admiral Markets for any future performance. The value of the financial instrument may both increase and decrease and the preservation of the asset value is not guaranteed.

- The projections included in the Analysis may be subject to additional fees, taxes or other charges, depending on the subject of the Publication. The price list applicable to the services provided by Admiral Markets is publicly available from the website of Admiral Markets.

- Leveraged products (including contracts for difference) are speculative in nature and may result in losses or profit. Before you start trading, you should make sure that you understand all the risks.