Investing in UK Tech Stocks

When people think of technology stocks, their minds inevitably turn to the US and industry giants such as Apple or Amazon. However, the UK market is also home to a number of smaller tech companies, each with its own risk profile and potential growth narrative. In this article, we’ll highlight 3 UK tech stocks, examine their recent performance and highlight some of the risks they face.

The information in this article is provided for educational purposes only and does not constitute financial advice. Consult a financial advisor before making investment decisions.

Table of Contents

Top UK Tech Stocks to Watch

Whilst the London Stock Exchange (LSE) may not be renowned for technology stocks, there are a number of options available to investors. Here are 3 top UK tech stocks which have performed well in their latest annual results and could be companies to watch in 2026.

Market capitalisation figures as of 14 April 2026. Please note market cap is subject to change on a daily basis. Past performance is not a reliable indicator of future results.

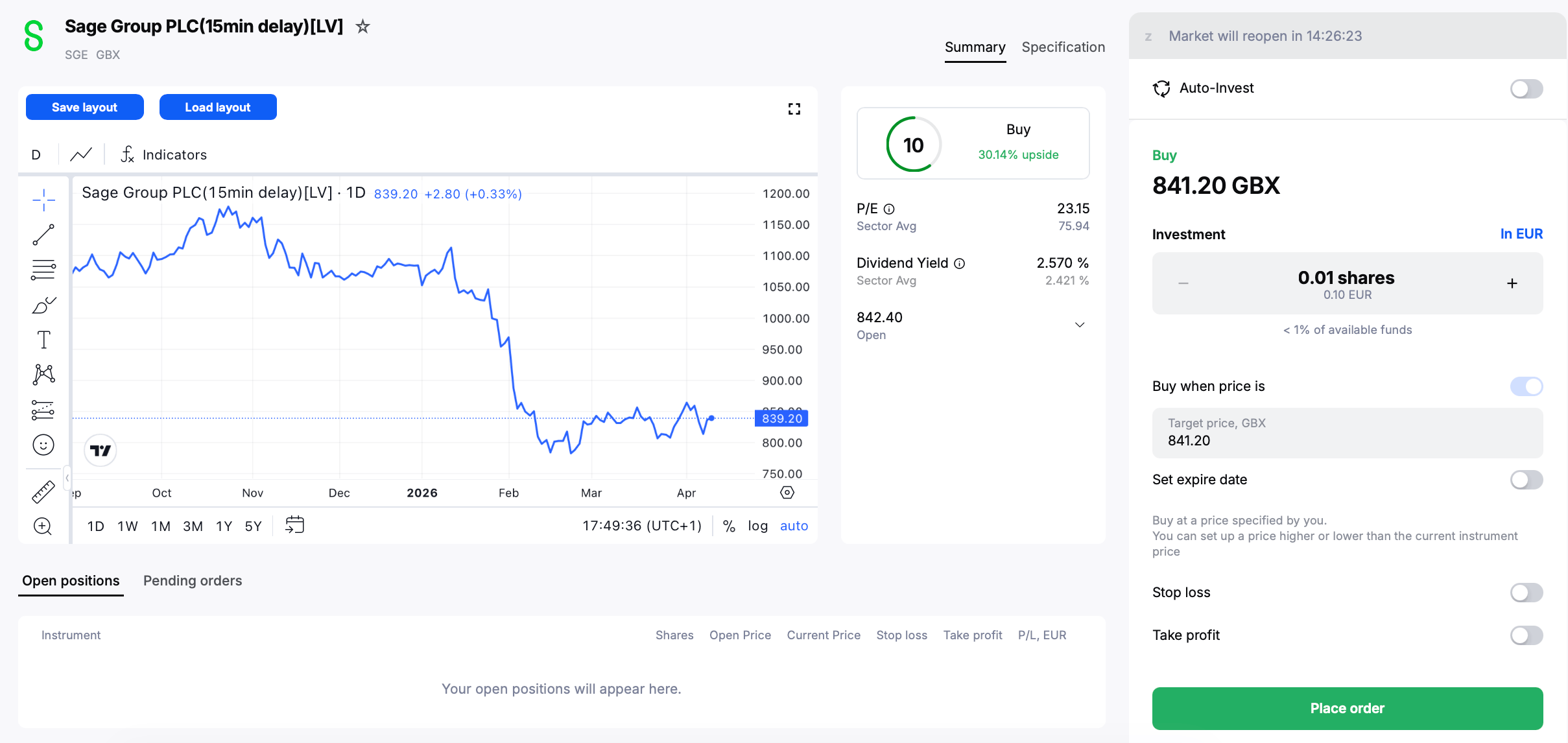

Sage Group

Founded in 1981, FTSE 100 constituent Sage Group is probably one of the most well-known UK tech companies.

It is a leading provider of business management and financial software, which helps organisations with operations such as accounting, payroll and HR.

Sage’s share price has come under pressure in recent months due to concerns about potential disruption from Artificial Intelligence (AI). Investors appear to be concerned about the effects AI tools could have on demand for software providers such as Sage.

However, its full-year 2025 results looked positive. In the year ended 30 September 2025, underlying revenue rose 10% to £2,513 million and underlying operating profit increased 17% to £600 million. Importantly, 97% of Sage’s total revenue was recurring thanks to Sage’s transition towards subscription and cloud services.

Recurring revenue refers to income generated from subscriptions, which can provide a relatively predictable stream of revenue (In FY25, Sage had a renewal rate, by value, of 101%).

Amongst other things, this predictable stream of revenue helps support Sage’s dividend payments, of which it has an impressive track record. Sage has increased its base dividend every year for more than two decades; however, future payouts are never guaranteed.

Computacenter

Computacenter is a technology services company which helps corporate and public sector organisations source, implement and manage their IT infrastructure. In other words, it generates income from services, consulting and hardware reselling as opposed to building its own technology or software.

Computacenter stands to potentially benefit from AI-related demand as organisations look to invest in new infrastructure. Indeed, in its annual report, Computacenter attributed high revenue growth in its Technology Sourcing segment to “buoyant demand for AI-related infrastructure”, particularly in North America, but also in the UK.

Nevertheless, this potential benefit also marks a potential risk, which is that the company is exposed to the cyclical nature of IT spending. An economic downturn could result in companies spending investing less in IT infrastructure, which may harm Computacenter’s earnings.

Technology Sourcing revenue jumped 41% to £7.5 billion in the year ended 31 December 2025. Services revenue grew more slowly, rising 3% to £1.7 billion, resulting in total revenue of £9.2 billion. Adjusted operating profit rose 11% to £275 million.

Computacenter has consistently paid dividends for more than 20 years. Although it cut its dividend in 2019, it has increased its payout every year since.

Raspberry Pi

Founded in 2012, Raspberry Pi is best known for its low-cost, high-performance single-board and modular computers, which are built on the Arm architecture and run the Linux operating system.

Although often associated with enthusiasts, it has a growing market in industrial and embedded applications. Indeed, whilst it started as an educational and hobbyist product, commercial customers now account for the majority of revenue.

In 2025, Raspberry Pi revenue rose 25% to $323 million, whilst operating profit rose 35% to $36 million.

CEO Eben Upton noted that edge AI – the deployment of AI models directly on local devices rather than in the cloud - “represents a significant opportunity for Raspberry Pi. Our platforms allow OEMs to deploy AI applications at the edge of the network, delivering improved latency, privacy and cost compared to cloud-hosted alternatives.”

Nevertheless, Raspberry Pi’s performance is dependent on continued demand from hobbyists and industrial clients. As a small company, a slowdown in demand for its products or increased competition could have a significant impact on share price.

How to Buy UK Tech Shares

If you’re interested in investing in UK tech stocks, here’s how you can get started:

- Register for an account with a broker that offers access to the UK stock market and complete the onboarding process.

- Log in to your account and open the trading platform.

- Search for the UK tech stocks you want to buy and open the instrument page.

- Create a new order, enter how many shares you wish to purchase and click Buy.

Other Articles You Might Be Interested In:

Frequently Asked Questions

What are UK tech stocks?

UK tech stocks are companies listed on the London Stock Exchange that operate in technology-related areas such as software, IT services and specialised electronics.

What are some examples of UK tech companies?

Examples of top UK technology companies include Sage Group, Raspberry Pi, Halma and Computacenter.

Do UK tech stocks pay dividends?

Some UK tech companies, particularly more established ones like Sage Group and Computacenter, do pay dividends. This is less common among younger or higher-growth tech stocks, which may reinvest profits back into the business instead.

What are the risks of investing in UK tech stocks?

Risks include slower growth compared to global peers, exposure to economic cycles (especially for IT services firms) and competition from larger international technology companies.

The given data provides additional information regarding all analysis, estimates, prognosis, forecasts, market reviews, weekly outlooks or other similar assessments or information (hereinafter “Analysis”) published on the websites of Admirals investment firms operating under the Admirals trademark (hereinafter “Admirals”) Before making any investment decisions please pay close attention to the following:

- This is a marketing communication. The content is published for informative purposes only and is in no way to be construed as investment advice or recommendation. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and that it is not subject to any prohibition on dealing ahead of the dissemination of investment research.

- Any investment decision is made by each client alone whereas Admirals shall not be responsible for any loss or damage arising from any such decision, whether or not based on the content.

- With view to protecting the interests of our clients and the objectivity of the Analysis, Admirals has established relevant internal procedures for prevention and management of conflicts of interest.

- The Analysis is prepared by an analyst (hereinafter “Author”). The Author Roberto Rivero is a contractor for Admirals. This content is a marketing communication and does not constitute independent financial research.

- Whilst every reasonable effort is taken to ensure that all sources of the content are reliable and that all information is presented, as much as possible, in an understandable, timely, precise and complete manner, Admirals does not guarantee the accuracy or completeness of any information contained within the Analysis.

- Any kind of past or modelled performance of financial instruments indicated within the content should not be construed as an express or implied promise, guarantee or implication by Admirals for any future performance. The value of the financial instrument may both increase and decrease and the preservation of the asset value is not guaranteed.

- Leveraged products (including contracts for difference) are speculative in nature and may result in losses or profit. Before you start trading, please ensure that you fully understand the risks involved.